FX

Carry Trade Stress, When FX Stops Absorbing Risk

Nov 27, 2025

Carry Trade Stress, When FX Stops Absorbing Risk

A structural read on G10 funding pairs, carry regimes, and the point where FX stops cushioning global risk.

The first crack in global risk rarely shows up in equities.

It appears quietly in the funding pairs.

When carry trades are working, FX cushions bad news. Rate differentials pay you to own risk, and funding currencies act as shock absorbers. When those differentials lose conviction, the same trades start amplifying stress instead of absorbing it.

This Insight looks at the carry complex as a structural risk signal, rather than a standalone trade:

the behaviour of AUD–JPY and NZD–CHF 3-month differentials through major stress regimes

the average carry pulse mapped directly against MSCI World drawdowns

Together, they show when FX is insulating the system and when it has flipped into transmission mode.

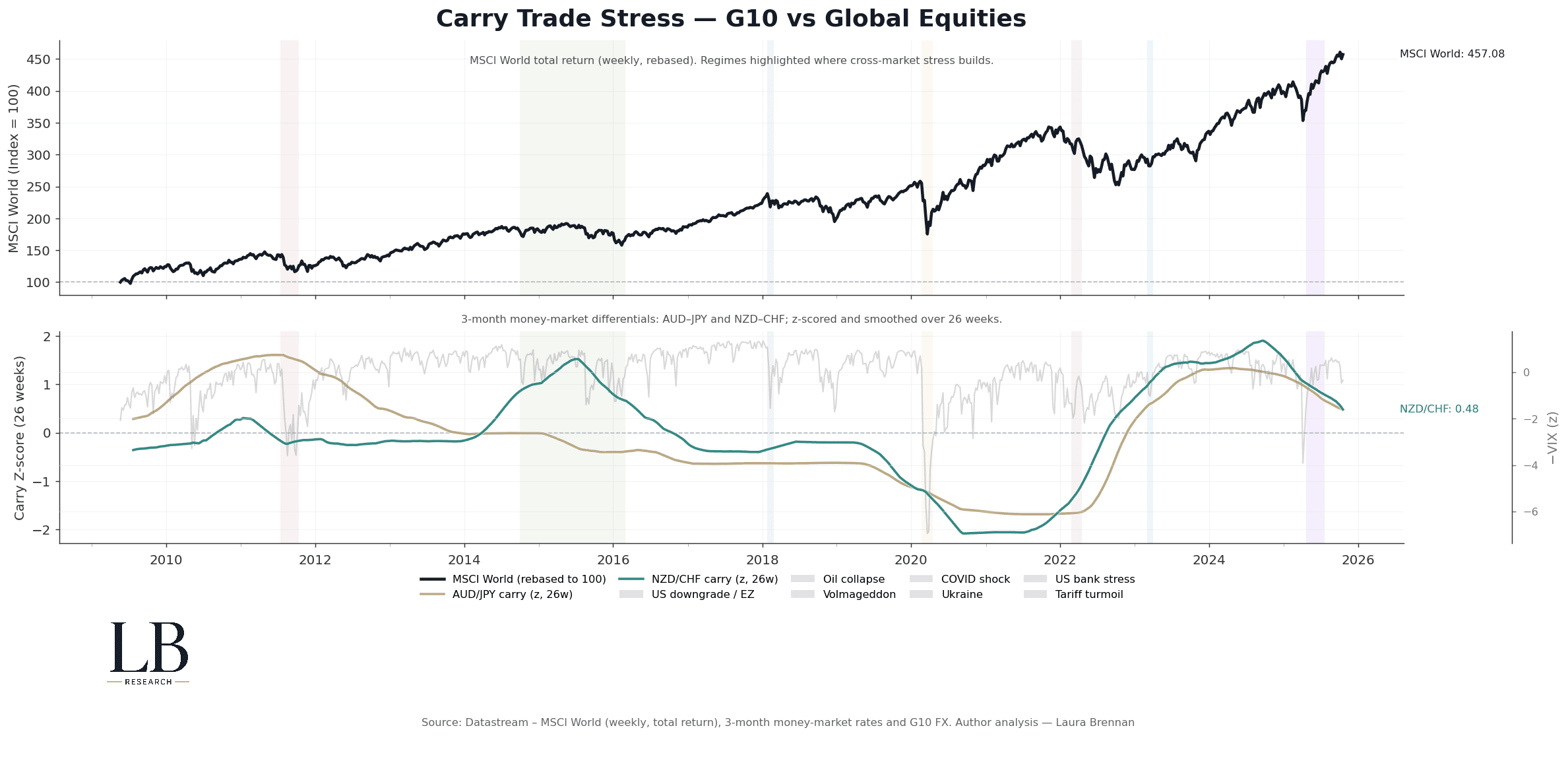

Carry as the First Crack

The top panel tracks MSCI World total return, rebased to 100 and shaded across major stress regimes – from the US downgrade and the Eurozone crisis through Oil Collapse, Volmageddon, COVID, and the 2022–23 rates reset.

The bottom panel plots:

AUD–JPY carry (z, 26 weeks)

NZD–CHF carry (z, 26 weeks)

a faint inverted VIX z-score, as a volatility backdrop

Both carry series are built from 3-month money-market differentials, z-scored and smoothed over 26 weeks to focus on regime shifts rather than day-to-day noise.

In normal conditions, at least one of the pairs sits comfortably positive. Funding currencies do their job: they finance risk and cushion shocks.

What stands out across the shaded regimes is how often both series roll over together before, or in the early stages of, major equity stress.

Carry behaviour across major stress periods. When both AUD–JPY and NZD–CHF turn negative together, global risk appetite is already under strain.

Regime Behaviour Across Stress Periods

AUD–JPY and NZD–CHF are not identical trades. One leans more towards Asia-Pacific growth and commodity risk; the other is closer to a high-beta vs low-beta European funding pair.

Yet, across the full history of the chart:

early cracks in risk show up as softening carry in one pair first

deeper episodes, such as the Euro crisis, COVID shock and the 2022–23 hiking cycle, see both pairs press lower together

the most acute phases coincide with a rise in inverted VIX and a clear deterioration in the FX cushion

By the time the MSCI line looks obviously stressed, the carry complex has usually been signalling discomfort for several weeks.

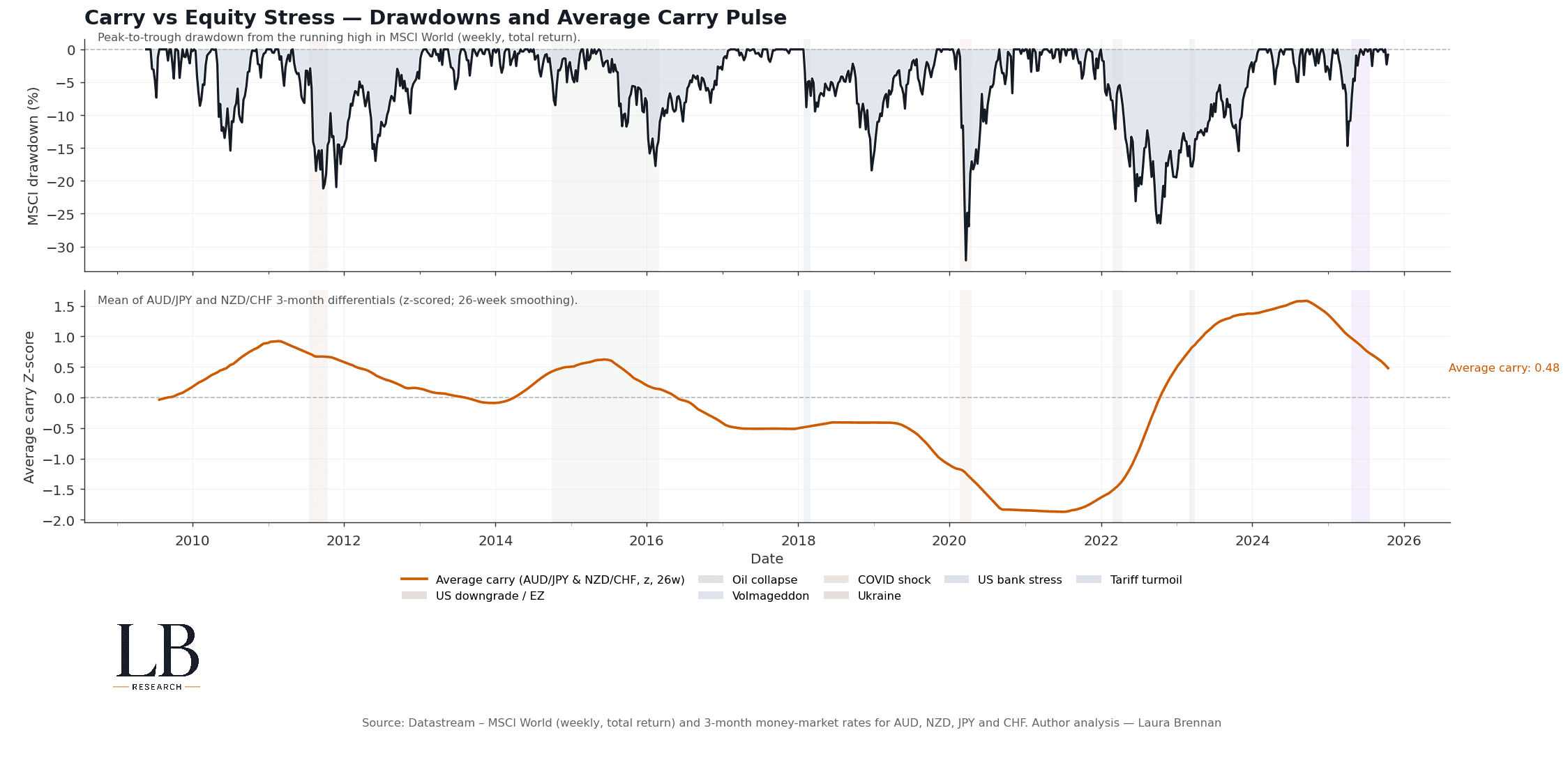

Carry vs Equity Drawdowns

To make that link explicit, the second figure maps:

Top panel: peak-to-trough drawdown from the running high in MSCI World (weekly, total return)

Bottom panel: the average carry pulse, defined as the mean of AUD–JPY and NZD–CHF 3-month differentials, z-scored and smoothed over 26 weeks

The drawdown panel shows the familiar profile: shallow pullbacks, occasional sharp air-pockets, and a handful of regime-level slumps.

The carry panel moves more slowly, but structurally. The deepest equity losses do not occur in isolation. They appear once the average carry pulse has already turned negative and stayed there.

Average carry pulse versus MSCI World drawdowns. Equities tend to deepen once FX has already withdrawn its cushion.

The Carry Pulse Today

On the latest reading, the average carry pulse has normalised back into positive territory, and both AUD–JPY and NZD–CHF sit within a moderate z-score band. The system currently has an FX cushion again: funding currencies are being paid to support risk rather than fight it.

History, however, suggests that stability here is conditional. Prolonged negative readings in the carry pulse have been a reliable backdrop for deeper equity drawdowns and higher cross-asset synchronicity.

This is why, at LB Research, FX carry is treated as a structural signal, not just a trade:

when carry is healthy and differentiated, risk can be selective

when carry compresses and both funding pairs roll over together, liquidity thins and drawdowns propagate faster

If you want the extended package

From this framework I can also publish:

a cross-market carry map across additional G10 pairs

a transition matrix of carry regimes into equity drawdown states

ETF-linked implementations via G10 FX, multi-asset carry baskets, or volatility overlays

Tell me which one you’d like to see next.