Correlation

Energy Stress and Cross-Asset Synchronisation

Apr 2, 2026

Energy Stress and Cross-Asset Synchronisation

When energy stress rises, markets begin to move as one.

Energy shocks do not remain contained within a single market.

They propagate across portfolios.

They act as a system-wide constraint, tightening financial conditions and compressing diversification across assets.

What follows is not simply higher volatility, but a shift in how markets behave.

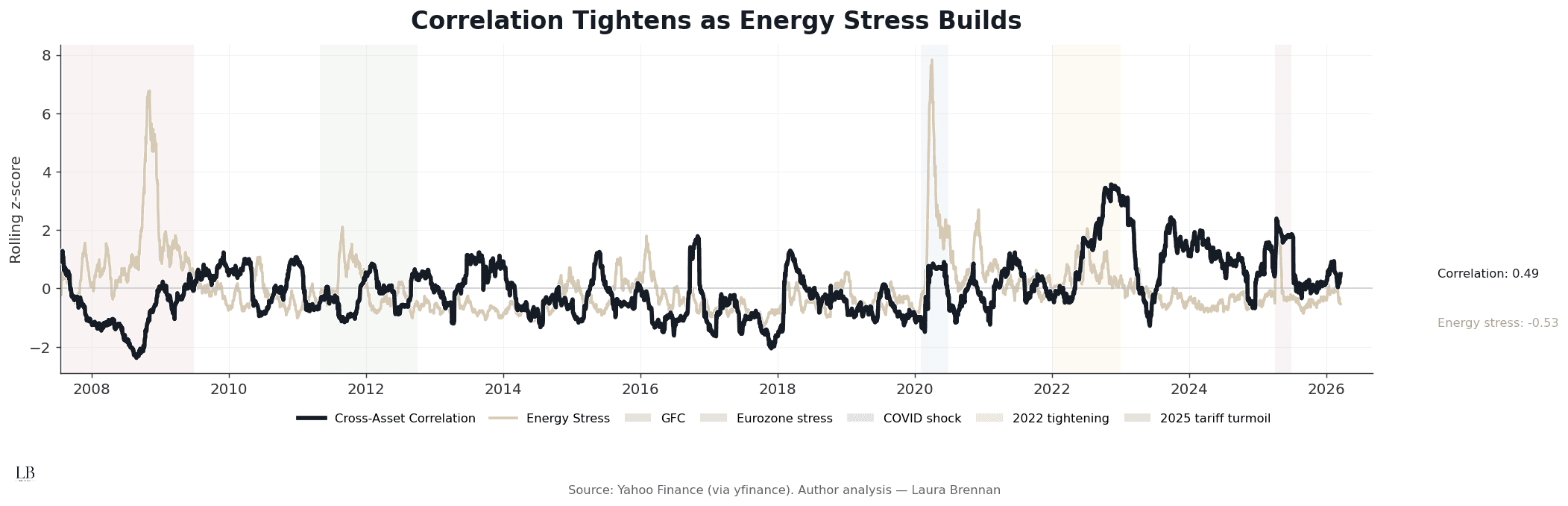

System Response: Correlation Tightening

Correlation rises as energy stress builds, signalling a loss of diversification.

Periods of elevated energy stress coincide with a steady increase in cross-asset correlation.

This reflects a transition from independent price behaviour to shared macro-driven movement.

As stress intensifies, assets that typically diversify portfolios begin responding to the same underlying forces.

Diversification does not disappear.

But its protective power weakens precisely when it is most needed.

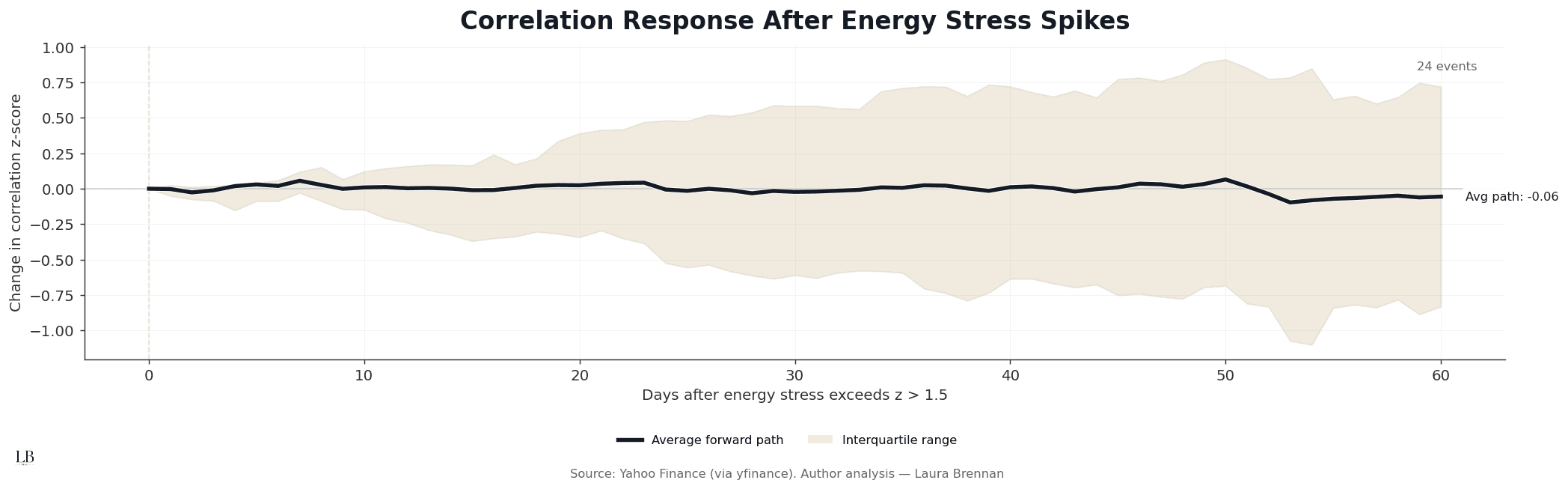

Timing: What Happens After a Shock

The response is not uniform. Dispersion increases even when the average effect appears muted.

Following energy stress spikes, correlation does not move in a single direction.

Instead, the range of outcomes widens.

• Some episodes show rapid synchronisation

• Others exhibit delayed or fragmented responses

• The average path masks significant variation

Stress introduces uncertainty not just in magnitude, but in how correlation evolves over time.

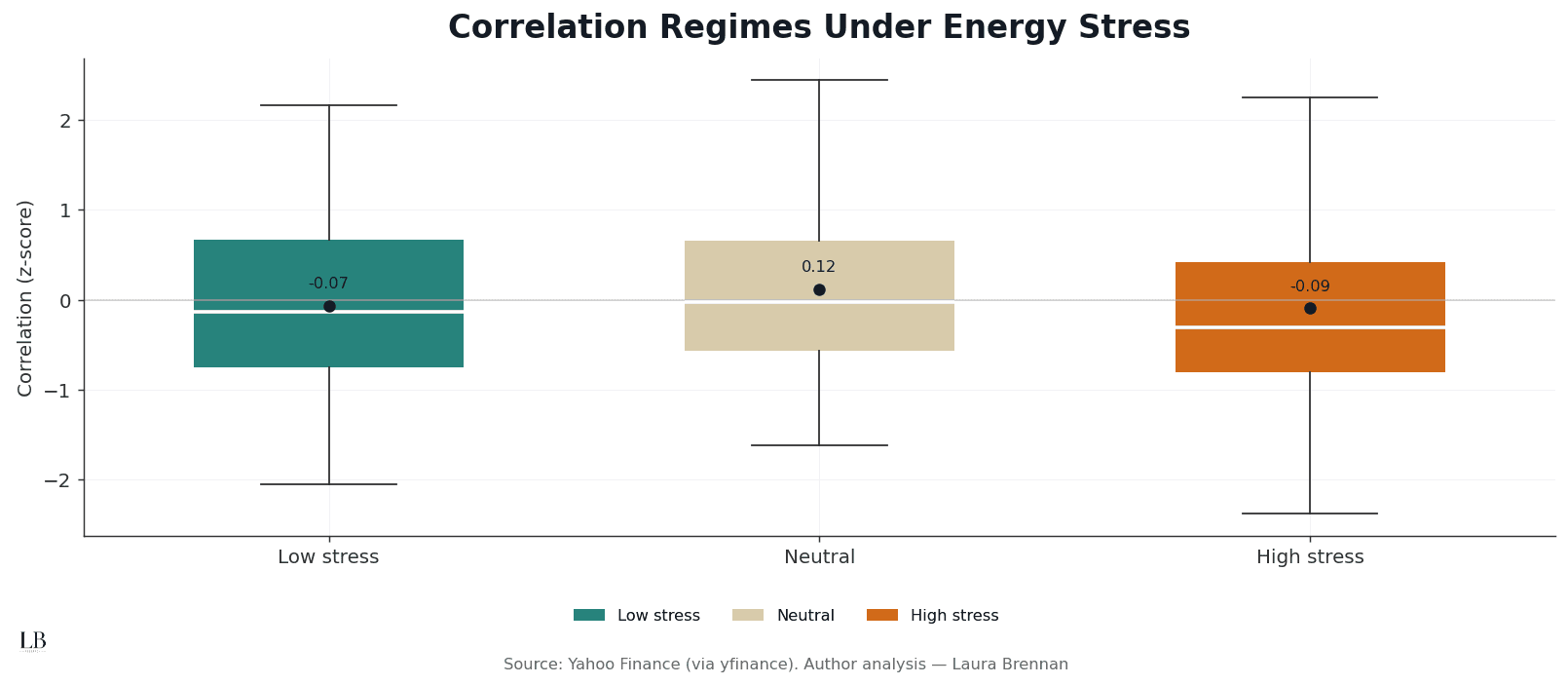

Regime Behaviour: Where Correlation Peaks

Correlation often peaks before stress becomes extreme.

The highest levels of synchronisation are not always observed during the most severe stress periods.

Instead, correlation tends to rise during transitional regimes, where positioning adjusts before stress fully materialises, where uncertainty builds but markets have not yet fully adjusted.

This suggests that diversification may begin to weaken ahead of visible crisis conditions, rather than at the point of maximum stress.

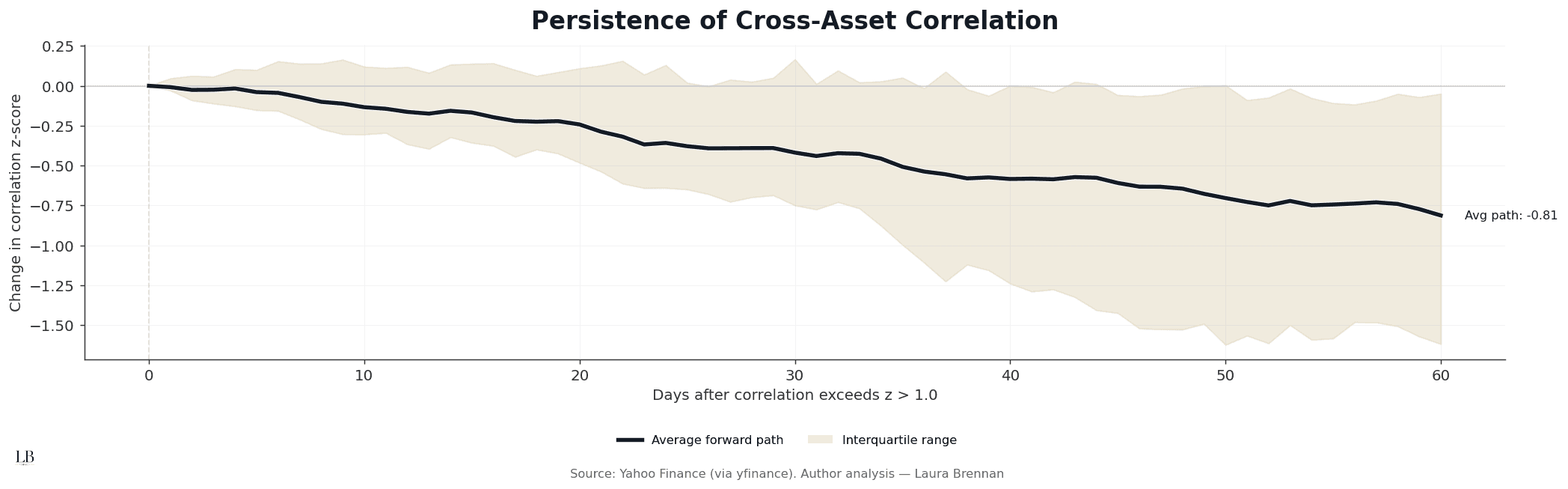

Persistence: Correlation Does Not Revert Immediately

Correlation shocks fade, but not instantly.

Once correlation rises, it does not revert immediately.

The adjustment is gradual and uneven, rather than a sharp reversal.

• Correlation declines over time rather than snapping back

• The unwinding process is slow and inconsistent

• Diversification returns, but with a lag

This persistence indicates that system-wide behaviour outlasts the initial shock.

Structural Interpretation

Across all dimensions, a consistent pattern emerges.

• Energy stress compresses diversification

• Cross-asset relationships tighten under constraint

• The response varies across time and regimes

• Recovery is gradual rather than immediate

Systemic risk is not simply higher volatility.

It is the loss of independence across assets.

When markets respond to shared constraints, diversification weakens not because assets become riskier in isolation, but because they begin reacting to the same forces at the same time.

Methodology

Assets: Cross-asset ETF universe (equities, bonds, commodities)

Proxy: Energy stress (oil and gas dynamics)

Correlation: 60-day rolling cross-asset correlation of returns

Normalisation: Z-score standardisation

Event study: Forward correlation paths following stress thresholds

Source: Market data (Yahoo Finance via yfinance)

Analysis: Laura Brennan