Systemic Risk

Liquidity Stress Turning Systemic

Mar 26, 2026

Liquidity Stress Turning Systemic

Cross-Asset Behaviour During Forced De-Risking

Key Observations

• Liquidity shocks force simultaneous portfolio deleveraging

• Cross-asset correlations rise as investors reduce exposure

• Volatility propagates across markets rather than remaining isolated

• Forced liquidation can generate severe market dislocations

Periods of systemic stress are characterised not only by rising volatility but by changes in the structural relationships between assets.

When liquidity conditions deteriorate, investors reduce risk across portfolios rather than within individual markets. As a result, assets that normally provide diversification begin reacting to the same liquidity constraints.

The following analysis examines how cross-asset relationships evolved during the 2020 liquidity shock.

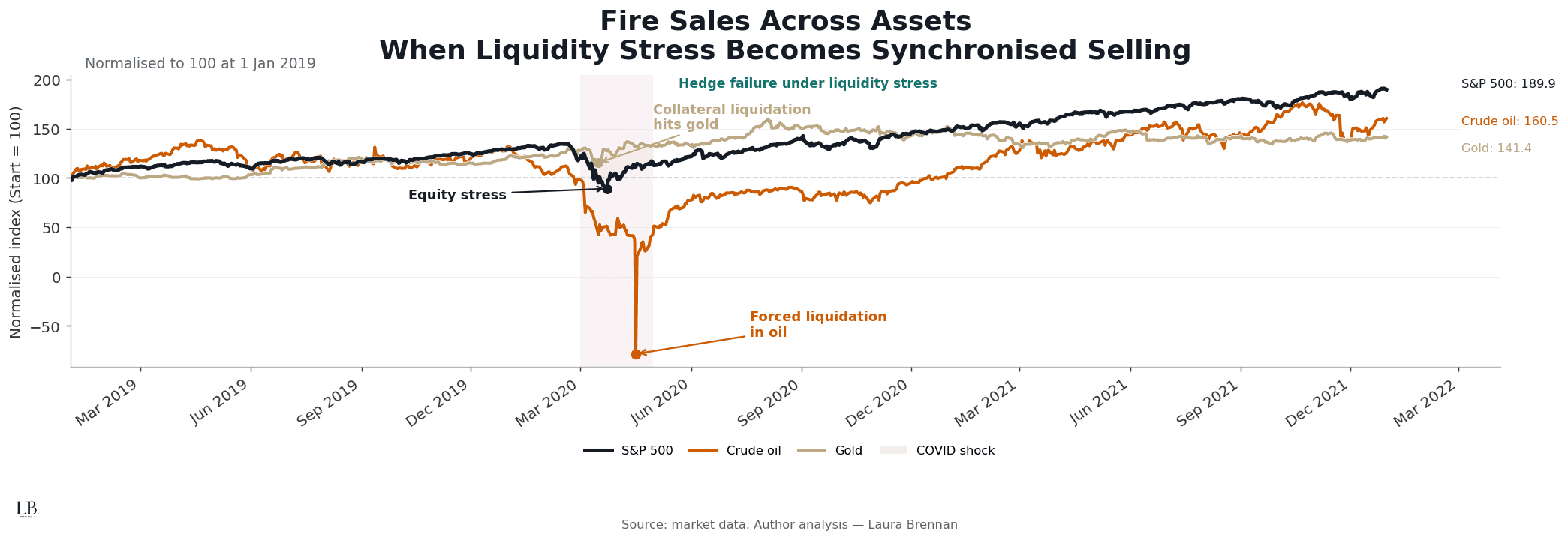

Cross-Asset Liquidation Dynamics

Synchronous selling during liquidity stress

Chart Insight

Liquidity shocks trigger portfolio-wide deleveraging across assets., causing assets that normally behave independently to decline simultaneously.

Observations

• Equity markets absorbed the initial phase of the shock

• Gold weakened temporarily as investors liquidated collateral

• Oil experienced extreme forced liquidation in futures markets

• Asset price movements became increasingly synchronised

These dynamics reflect portfolio-level de-risking rather than independent asset-specific shocks.

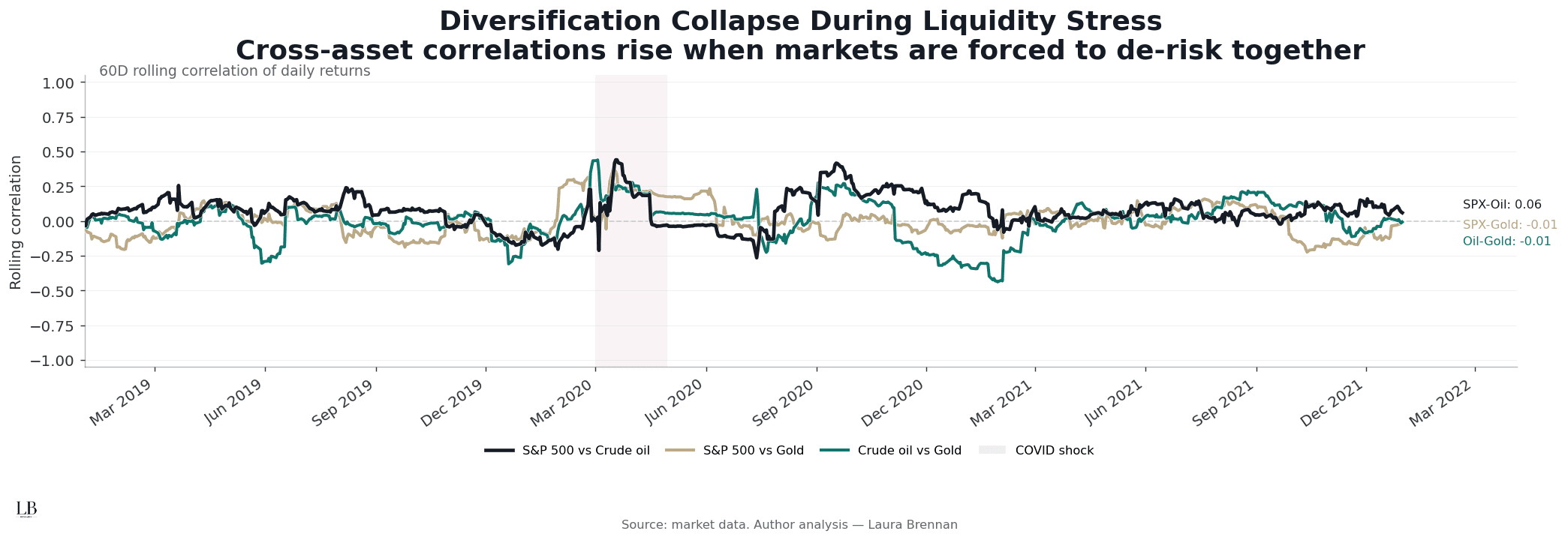

Diversification Breakdown Under Forced De-Risking

Cross-asset correlations during stress regimes

Chart Insight

Diversification weakens during liquidity shocks as cross-asset correlations rise sharply.

Observations

• Cross-asset correlations increase during the crisis period

• Assets that typically diversify portfolios begin moving together

• Correlation spikes coincide with periods of liquidity stress

• Portfolio diversification deteriorates as de-risking accelerates

These patterns illustrate how diversification can weaken precisely when it is most required.

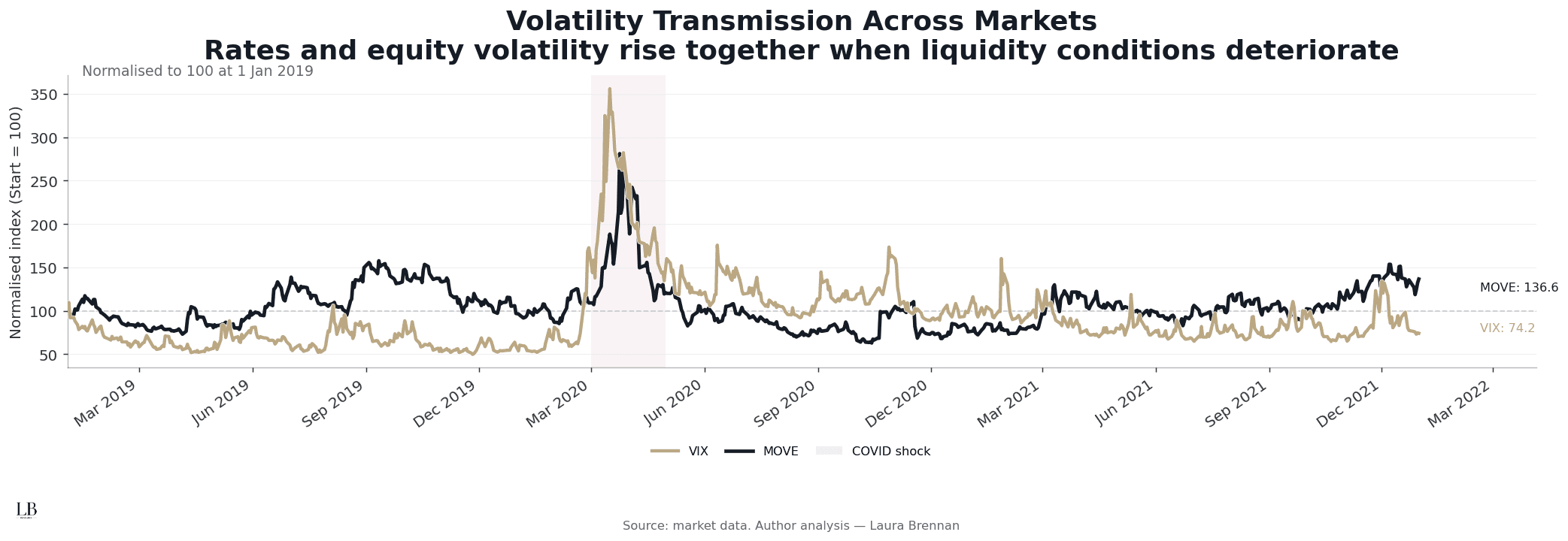

Volatility Transmission

Propagation of stress across asset classes

Chart Insight

Volatility does not remain confined to a single market during crises; it propagates across asset classes as systemic stress intensifies.

Observations

• Equity and rates volatility spike simultaneously during the crisis

• Liquidity tightening transmits volatility across markets

• Stress spreads beyond equities into fixed income markets

• Elevated volatility persists after the initial shock

This behaviour is consistent with systemic tightening in global financial conditions.

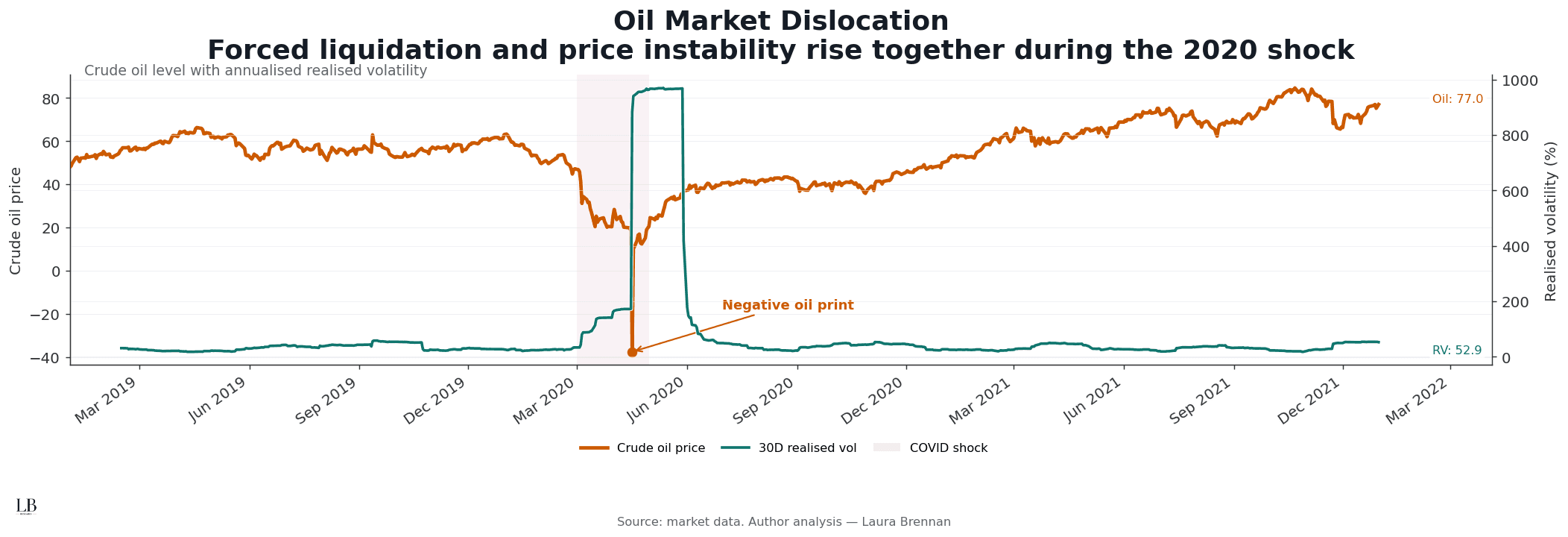

Market Dislocation: Oil Futures

Forced liquidation and price instability

Chart Insight

Extreme price dislocations can emerge when leveraged positions are unwound under severe liquidity pressure.

Observations

• Oil prices collapsed during the liquidity shock

• Realised volatility surged to unprecedented levels

• Futures markets experienced forced liquidation

• Prices briefly traded below zero

This episode illustrates how market structure can break down when participants are forced to liquidate positions regardless of price.

Structural Interpretation

Across these perspectives, a consistent pattern emerges.

• Liquidity shocks trigger simultaneous portfolio deleveraging

• Cross-asset correlations increase as diversification erodes

• Volatility propagates across markets

• Forced liquidation can destabilise market structure

Systemic risk is therefore not defined solely by volatility.

It reflects the loss of independence across assets when financial markets respond to shared liquidity constraints.

Methodology

Assets: S&P 500, crude oil, gold

Volatility measures: VIX (equities), MOVE (US Treasury volatility)

Frequency: Daily observations

Correlation measure: 60-day rolling correlations of daily returns

Realised volatility: 30-day rolling standard deviation of returns (annualised)

Normalisation: Series indexed to 100 at 1 January 2019

Source: Market data

Analysis: Laura Brennan